What is Original Medicare?

Original Medicare is the United States’ federal health insurance program for people who are 65 or older. It is also available for certain people younger than 65 with disabilities or people with End-Stage Renal Disease. There are several parts to Medicare that contain different coverage.

What is Part A?

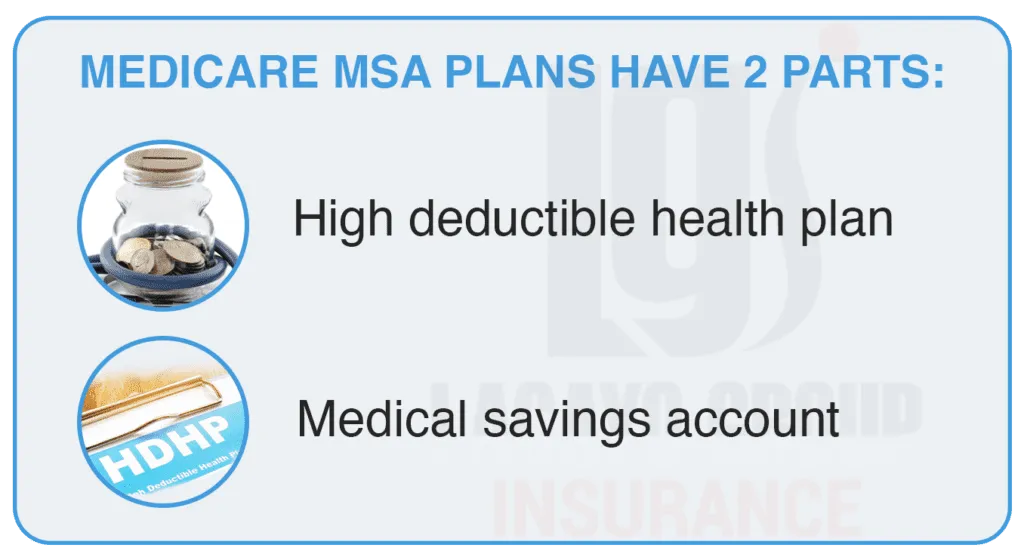

MSAs have two parts by combine a high-deductible insurance plan with a medical savings account to pay for your health care costs. You're responsible for handling the money in your account, including deciding whether to pay for health care services using your account funds or other funds you have.

1. High-deductible health plan: This is a special type of Medicare Advantage Plan. This type of plan only starts to cover your costs once you meet a high yearly deductible, which varies by plan.

2. Medical savings account (MSA): This is a special type of savings account. Medicare gives the plan an amount of money each year for your health care expenses. This amount is based on your plan. The plan deposits money into your MSA account once at the beginning of each calendar year. Or, if you become entitled to Medicare in the middle of the year and join a Medicare MSA Plan at that time, the plan will deposit the money into your account the first month your coverage starts.

You can use this money to pay your Medicare-covered costs before you meet the plan’s deductible. You can access the money using a checking account or special debit or credit card your bank gives you. The yearly deposit and yearly deductible are pro-rated based on when your enrollment begins.

How Do Medicare MSA's Work?

MSA plans are sold by private insurance companies that contract with banks to arrange the savings accounts. Medicare places a specific amount of money into your account at the beginning of each year. The deposited money is tax-exempt, and you can withdraw it from your MSA, tax-free, so long as you use it for approved medical expenses.

Is a Medicare MSA a Good Choice?

Medicare MSA are more like a self-directed health insurance plan than a managed Medicare Advantage program. The money deposited into someone’s account is yours to keep when you stay in the plan. And it goes with you, just like how an employer-plan HSA is portable.

Disabled Medicare beneficiaries (under 65) can get good protection from an MSA. But an MSA plan can also be attractive for healthy Medicare recipients with zero chronic health conditions. You’ll want to look at the plan’s annual deductible, but it may cover MOST routine spending for healthy applicants. Therefore, MSAs are a cheaper way to insure against dire health risks.

Don't Risk Getting the Wrong Coverage

Work with the Best!

We understand the Medicare enrollment process can be difficult to

understand. This is why we strive to educate and empower our clients to

make the best decisions for their health insurance coverage.

MSA's Are Now Available Wyoming

If you or your spouse ever worked for an employer who is a member of your local Wyoming Chamber of Commerce, you and your family now have access to the Medicare MSA option. This unique opportunity extends to members, employees, former employees, and even eligible spouses. It’s another way Chambers of Commerce are helping their communities access flexible Medicare coverage not widely available in Wyoming.

Current Participating Chambers of Commerce Include:

Cody, Casper, Riverton, Lander, Campbell County, and Evanston

Grab Our Free

Comprehensive Guide to Medicare!

Medicare can be a nightmare to understand. I’ve helped thousands of Baby Boomers navigate this journey and I hope this book can help you too!